Owing money can quickly turn into a stressful situation, especially when you’re unsure about what steps you can take to get paid back. If someone owes you money, you might feel stuck, frustrated, or even powerless.

But the truth is, you have legal options to protect your rights and reclaim what’s yours. Whether it’s a friend, family member, or business associate, knowing what you can do legally puts you back in control. Keep reading to discover clear, practical steps you can take—from simple reminders to formal court actions—that will help you handle this challenge confidently and effectively.

Your money matters, and it’s time to make sure you get it back.

Gathering Proof

Gathering proof is the first and most important step when someone owes you money. Proof shows the debt is real and helps you in legal actions. Without proof, your claim may be weak or ignored. Collecting clear, organized evidence makes your case stronger and faster to resolve.

Collecting Documents

Start by gathering all documents related to the loan or debt. Look for signed contracts, promissory notes, or written agreements. Include receipts, bank statements, or cancelled checks that show money was lent or paid. Emails and text messages with payment terms or promises to pay also count as proof. Keep copies safe and organized for easy access.

Recording Communication

Keep a detailed record of all communication with the person who owes you money. Write down dates, times, and what was said during phone calls or meetings. Save text messages, emails, and any letters you send or receive. If you talk in person, follow up with a written summary by email. These records show your efforts to collect the debt and prove the person acknowledged it.

Informal Contact

Informal contact is the first and simplest step to recover money owed. It involves direct communication without legal actions. This approach often saves time and costs. It helps maintain good relationships while trying to solve the issue.

Starting with informal contact can encourage the debtor to repay willingly. Clear and polite communication sets a positive tone. It can lead to a solution without escalating the matter.

Polite Reminders

Sending polite reminders is a gentle way to prompt repayment. A simple message or call can remind the person of their debt. Keep the tone friendly and respectful. Avoid blaming or threatening language.

Reminders can be spaced out over time. This shows patience and understanding. It increases the chance that the debtor will respond positively.

Negotiating Payment Plans

Sometimes debtors cannot pay the full amount at once. Offering a payment plan helps both sides. Agree on smaller, manageable payments over a set period. Write down the plan details to avoid confusion.

Negotiation shows you are willing to find a fair solution. It encourages cooperation and builds trust. This method often leads to full repayment without legal steps.

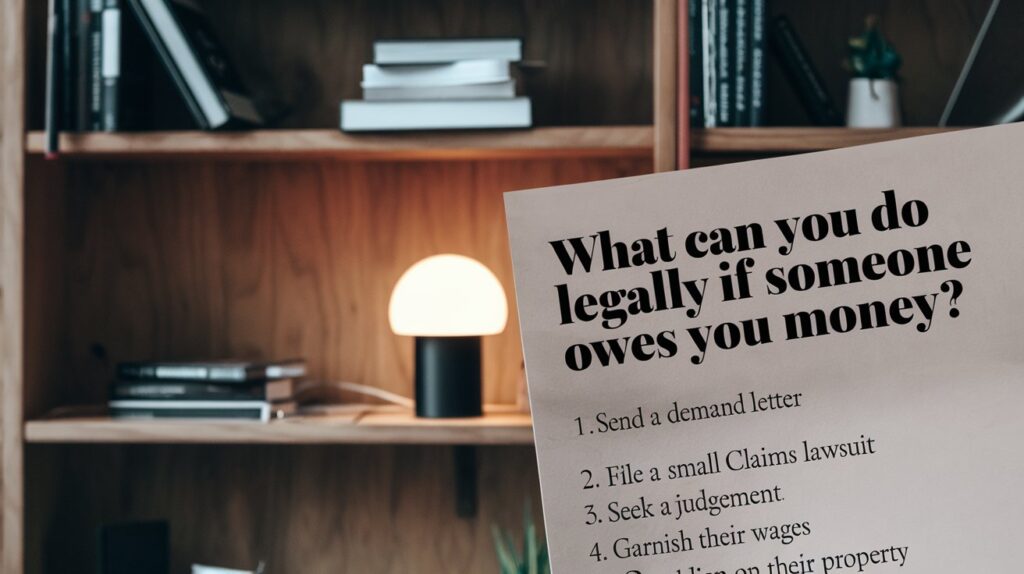

Sending A Demand Letter

Sending a demand letter is a key step when someone owes you money. It is a formal written request for repayment. This letter shows you are serious about recovering your funds. It also creates a paper trail for future legal actions. Many debtors respond quickly to a clear, polite demand letter.

A demand letter explains how much is owed and when payment is expected. It can prevent misunderstandings and encourage timely repayment. Writing one properly increases your chances of getting paid without court involvement.

What To Include In A Demand Letter

Start by stating your name and contact details clearly. Mention the debtor’s full name and contact information. Describe the debt amount and the reason for the loan or transaction. Include dates when the money was lent and any agreed repayment terms.

Request payment by a specific deadline. Offer payment options if possible. Mention consequences of not paying, such as legal action. Keep your tone professional and firm but polite.

How To Send A Demand Letter

Send the letter via certified mail with a return receipt. This proves the debtor received it. You may also send it by email or hand delivery, but certified mail is best for legal proof. Keep copies of the letter and all mailing receipts. This documentation helps if you later go to court.

Benefits Of Sending A Demand Letter

A demand letter often motivates debtors to pay faster. It shows you know your rights and are ready to act. Courts may require proof of a demand letter before hearing a case. It can save time and money by avoiding lengthy legal proceedings. Many disputes resolve after this simple step.

Mediation Options

Mediation is a way to solve money disputes without going to court. It involves a neutral third party who helps both sides reach an agreement. This option can save time, money, and stress compared to a trial.

Many courts encourage or require mediation before a case proceeds. Mediation focuses on cooperation and finding a solution that works for both parties. It can be used in many types of money disputes, including loans and unpaid bills.

Court-ordered Mediation

Court-ordered mediation means the court requires you to try mediation before continuing your case. The judge appoints a mediator to guide the discussion. Both parties must attend and try to reach a settlement.

This process helps reduce the court’s workload. It gives a chance to solve problems quickly. If mediation fails, the case moves forward to court.

Benefits Of Mediation

Mediation is faster than going to court. It usually costs less because there are fewer fees. You keep control over the outcome rather than leaving it to a judge.

The process is private, unlike court trials which are public. It helps maintain good relationships between people. Mediation focuses on cooperation, not winning or losing.

Filing In Small Claims Court

Filing in small claims court offers a straightforward way to recover money owed to you. This legal option is designed for disputes involving smaller amounts. It allows individuals to represent themselves without hiring a lawyer, making it accessible and cost-effective. The process is quicker than regular court cases, helping you resolve the issue efficiently.

Understanding how to prepare and what to expect in court improves your chances of success. Being organized and clear about your claim helps the judge see your side of the story. Small claims court can be an effective tool to enforce repayment and protect your rights.

Preparing Your Case

Start by gathering all evidence related to the debt. Include contracts, receipts, messages, or any proof of the loan and payment attempts. Organize these documents clearly for easy presentation. Write a simple timeline explaining the key events. Be ready to explain why the money is owed and how much. Prepare a brief statement to present your case calmly and clearly.

What To Expect In Court

The court session is usually informal. Both parties will have a chance to speak and present evidence. The judge may ask questions to understand the situation better. Expect to explain your claim simply and answer any questions. The judge will make a decision based on the facts presented. If you win, the court can order the debtor to pay you back. Remember to stay respectful and focused during the hearing.

Civil Court Lawsuits

Civil court lawsuits provide a formal way to recover money owed to you. This legal route involves filing a case against the person who owes you money. The court reviews the evidence and decides if repayment is required. It suits situations where informal methods have failed. The process can be time-consuming and might involve court fees. Understanding when to use civil court and whether to hire an attorney helps you make the best choice.

When To Choose Civil Court

Choose civil court if the debt is clear and the amount is significant. It works well when the debtor refuses to communicate or repay. Civil court suits are ideal for debts that exceed small claims limits. Use this option if you have solid proof of the loan and repayment terms. This method enforces your right to get paid through a legal judgment.

Hiring An Attorney

Hiring an attorney can improve your chances of success. A lawyer understands court rules and legal procedures. They help prepare your case and gather evidence properly. Attorneys negotiate with the debtor on your behalf to seek repayment. Legal counsel is useful if the case is complex or the amount is large. They guide you through the process to avoid costly mistakes.

After Winning A Judgment

After winning a judgment, your legal rights to collect money improve significantly. The court officially recognizes that the debtor owes you the specified amount. This judgment becomes a powerful tool to enforce repayment. Understanding your role and responsibilities helps you move forward effectively. Knowing what you can do next is crucial to recovering your money.

Understanding Judgment Debtor

The judgment debtor is the person or entity that owes you money. The court order requires them to pay the debt. Sometimes, the debtor might avoid payment or delay it. Knowing who the debtor is and their financial situation matters. This knowledge helps you choose the best enforcement actions. The debtor’s assets and income are important in this process.

Enforcement Responsibilities

Winning a judgment does not guarantee immediate payment. You must take steps to enforce the judgment. Common methods include wage garnishment, bank account levies, or property liens. Each method requires following legal procedures carefully. You may need to work with the court or a collection agency. Keep detailed records of all enforcement actions. Persistence and patience often lead to successful recovery.

Enforcing Payment

Enforcing payment means using legal methods to get money owed. Courts can help you collect money after a judgment. The process ensures debtors pay what they owe.

Different tools exist to enforce payment. These include taking money from wages, bank accounts, or property. Each option has specific rules and limits.

Wage Garnishment

Wage garnishment lets you take money directly from a debtor’s paycheck. The court orders the employer to withhold a portion of wages. This amount goes to you until the debt clears.

Limits exist on how much can be taken from wages. The law protects a portion of income for living expenses. Garnishment continues until the full debt is paid or the court stops it.

Bank Account Levy

A bank account levy freezes and takes money from the debtor’s bank account. The court issues the levy after you win a judgment. The bank must hold or turn over funds to satisfy the debt.

This method helps collect money quickly. Banks notify the debtor of the levy, giving them time to respond. Some funds, like Social Security, may be protected and not taken.

Property Liens

A property lien places a legal claim on the debtor’s real estate or personal property. It prevents the debtor from selling or refinancing without paying the debt. Liens stay until the debt is paid or the court removes them.

Liens give you security and priority over other creditors. They help ensure the debtor pays before selling valuable property. This method works well for large debts tied to assets.

Limitations Of Police Involvement

Police involvement in money disputes has clear limits. Owing money is usually a civil matter, not a criminal one. Police generally do not get involved in debt collection cases. Understanding when police can act helps avoid false expectations.

Legal action to recover money often requires court procedures. Police may only assist after a court decision orders repayment or property return. Knowing these boundaries guides you to the right steps for getting your money back.

When Police Can Intervene

Police can act if there is clear evidence of a crime. Examples include theft, fraud, or scams related to money owed. Simple failure to pay a debt does not qualify as a crime. Police need proof that the debtor intended to steal or cheat.

Police may also help enforce court orders. If a court has ruled that money must be paid, police or sheriffs can assist in enforcing that order. Without such a court order, police usually cannot force repayment or seize property.

Court Orders And Enforcement

The court system handles money disputes through civil cases. You must file a claim in court to prove the debt. If the court agrees, it issues an order requiring the debtor to pay.

Once a court order exists, enforcement can involve police or sheriff deputies. They can help seize property or garnish wages to satisfy the debt. Without a court order, these enforcement actions are not possible.

Understanding these rules helps you take the proper legal path. It avoids wasting time on police reports that will not lead to repayment.

Avoiding Legal Trouble

Dealing with money owed can be stressful. Staying within legal boundaries is crucial. Taking the right steps avoids trouble and protects your rights. Understand what actions are lawful and which are not. Knowing the law helps you handle debt issues wisely.

No Criminal Charges For Unpaid Debt

Not paying a debt is usually a civil matter. It is not a crime to owe money. The police do not get involved in unpaid debts. Legal action must go through the courts. Only a judge can order repayment or penalties. Avoid threats or harassment to prevent legal issues.

Intent And Repayment Obligations

Intent matters in debt cases. Courts look at whether the borrower planned to repay. If they meant to pay but could not, it is not fraud. Fraud involves knowingly lying or cheating to avoid payment. Keep clear records of all agreements and payments. This shows good faith and supports your claim.

Special Situations

-

Personal Loans: Require strong evidence (e.g., promissory note) for enforceability.

-

Business Debts: Use Uniform Commercial Code (UCC) for secured transactions (e.g., UCC § 9-609).

-

Interest: Charge reasonable interest if agreed (usury laws cap rates, e.g., 10–18% in many states).

-

International Debtors: Harder; may need Hague Convention service or foreign judgment enforcement.

Risks and Considerations

-

Counterclaims: Debtor may sue for harassment or invalid debt.

-

Costs: You may pay upfront fees, recoverable if you win.

-

Emotional Toll: Legal action strains relationships—consider if worth it for small amounts.

-

Statute of Limitations: Act before time runs out (e.g., 6 years for written contracts in many states).

Practical Tips

-

Document Everything: Keep records of agreements, payments, and communications.

-

Start Small: Use demand letters and small claims for efficiency.

-

Seek Free Help: Legal aid societies or state bar referrals for low-income individuals.

-

Avoid Illegal Tactics: No harassment, threats, or self-help repossession without court order (Fair Debt Collection Practices Act, 15 U.S.C. § 1692).

-

Prevent Future Issues: Use written contracts with clear terms for loans or services.

Frequently Asked Questions

What To Do If Someone Won’t Give You The Money They Owe You?

Start by politely reminding them and requesting repayment. Keep all proof of the debt. Send a formal demand letter if needed. Consider mediation to resolve disputes. If unpaid, file a claim in small claims court for legal enforcement. Consult a lawyer for complex cases.

Can You Go To The Police If Someone Owes You Money?

You cannot involve police just because someone owes you money. Police handle criminal cases, not civil debts. Use legal channels like demand letters, mediation, or small claims court to recover money owed. Court judgments may enforce repayment with sheriff assistance, not police action.

What To Do If Someone Doesn’t Pay Back Your Money?

Start by politely reminding the person and requesting repayment. Keep all loan records as proof. Send a formal demand letter if needed. Consider mediation to resolve disputes. If unpaid, file a claim in small claims court or consult a lawyer for legal action.

Can You Get In Legal Trouble For Not Paying Someone Back?

You typically won’t face criminal charges for not repaying a debt. Legal trouble arises only if intent to defraud existed. Lenders must pursue civil actions to recover money owed.

Conclusion

Taking legal steps can help you recover money owed. Start with clear communication and keep records safe. Sending a formal demand letter often prompts repayment. If the debt remains unpaid, small claims court offers a simple solution. Always know your rights and stay calm throughout the process.

Acting early increases your chances of success. Remember, patience and persistence matter most in these situations.

References

- Fair Debt Collection Practices Act, 15 U.S.C. § 1692 (2026).

- Uniform Commercial Code § 9-609 (2026).

- American Bar Association. Consumer Debt Collection Guide.

- Consumer Financial Protection Bureau. (2026). Debt Collection Rights.

Disclaimer: The content on this page is for general information only and should not be considered legal advice. We work hard to provide accurate and up-to-date details, but we can't guarantee the completeness or accuracy of the information. Laws and rules change often, and interpretations may vary. For specific advice, always consult a qualified legal expert. We are not liable for any actions you take based on this information. If you spot any errors or outdated content, please contact us, and we’ll update it as soon as possible.