Are you curious about how some businesses manage to pay less in taxes? You might have heard the term “tax haven” and wondered what it really means for companies like yours.

We’ll dive into the world of tax havens, unraveling their appeal and the legal landscape surrounding them. But it’s not all sunshine and savings; there are risks that every business owner should be aware of. Understanding these can help you make informed decisions about your business’s financial future.

Stick with us as we explore the intriguing, and sometimes controversial, role of tax havens in the global economy. Your knowledge of this topic could be the key to unlocking new opportunities—or avoiding potential pitfalls.

Tax Haven Definition

Have you ever thought about how businesses manage to keep their taxes low? The term “tax haven” often pops up in such discussions. But what exactly is a tax haven, and how does it affect businesses? Understanding the tax haven definition is crucial for anyone interested in international business or finance.

What Is A Tax Haven?

A tax haven is a country or territory where taxes are levied at a very low rate or not at all. It attracts businesses and individuals looking to reduce their tax liabilities. Tax havens offer financial privacy and favorable legal frameworks. They are often small countries with stable governments and economies.

Many businesses use tax havens to legally reduce their tax burdens. They register subsidiaries or conduct operations in these jurisdictions. However, it’s not just about paying less tax. It’s also about maximizing profits and ensuring business growth.

Tax havens typically have no or low income tax rates. They also provide minimal financial transparency. The legal systems in these countries are designed to attract foreign investment. They often have strict confidentiality laws.

Some tax havens offer specific benefits like no capital gains tax or inheritance tax. These features make them attractive to wealthy individuals and corporations. They provide a safe haven for assets, away from the prying eyes of tax authorities.

Examples Of Tax Havens

Countries like Bermuda, Cayman Islands, and Panama are well-known tax havens. These places have become popular for their favorable tax laws. Other examples include Monaco, Luxembourg, and the British Virgin Islands.

Businesses often set up shell companies in these jurisdictions. This allows them to manage profits and minimize tax liabilities. But is it worth the risk? What impact does this have on global economies?

Is Using A Tax Haven Legal?

Using a tax haven is legal, but it can be complicated. It’s crucial to understand the legal implications and requirements. Tax planning must adhere to international laws and regulations.

Businesses often hire legal experts to navigate these complexities. They ensure compliance with both local and international tax laws. But what happens if a company crosses the line? The risks can be significant.

Risks Of Using Tax Havens

While tax havens can offer benefits, they also come with risks. Companies may face reputational damage if accused of tax evasion. There’s also the risk of stricter regulations and penalties from their home countries.

Governments worldwide are cracking down on tax avoidance. They are implementing measures to prevent misuse of tax havens. So, is the short-term gain worth the long-term risk? It’s a question every business must consider.

As you explore the concept of tax havens, think about the broader implications. How do these practices affect global economies and tax fairness? Are businesses jeopardizing ethical standards for profit?

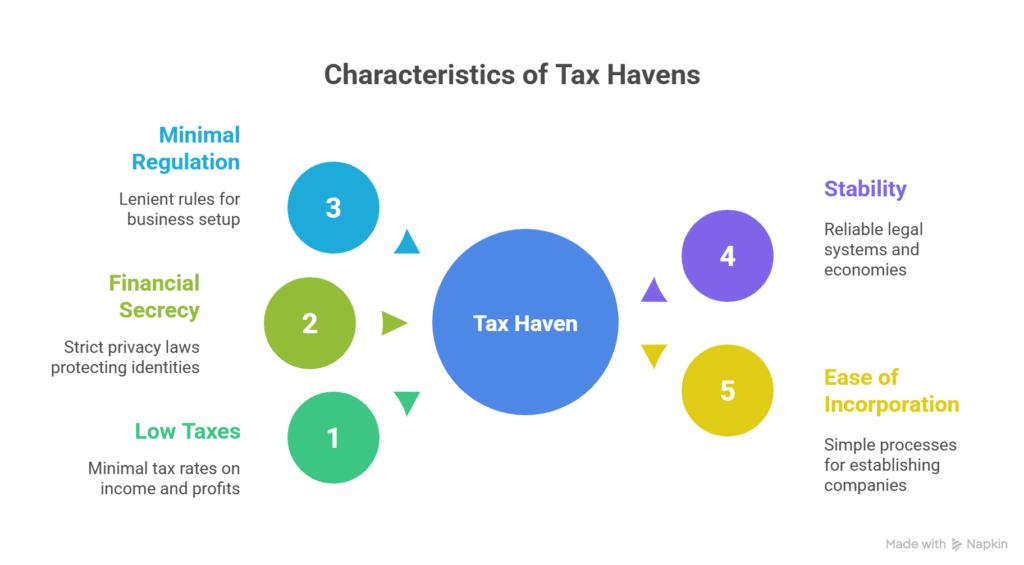

Characteristics Of Tax Havens

Tax havens offer low taxes and financial secrecy, attracting businesses seeking to reduce tax liabilities. They operate legally but pose risks like reputational damage and regulatory scrutiny. Companies must weigh potential savings against these risks.

Understanding the characteristics of tax havens can be crucial for businesses exploring international opportunities. These jurisdictions, often enticing due to their financial advantages, hold unique traits that differentiate them from other regions. As you navigate the complexities of global business, it’s essential to recognize what makes a tax haven stand out.

Low Or No Taxes

Tax havens are renowned for their low or non-existent tax rates. This characteristic attracts businesses aiming to maximize profits by minimizing tax liabilities. In some places, you might find corporate tax rates as low as 0%, which can significantly boost your bottom line. However, it’s wise to consider the ethical and reputational implications of utilizing such jurisdictions. Does the allure of tax savings outweigh potential scrutiny from stakeholders?

Financial Secrecy

Another hallmark of tax havens is their stringent financial secrecy laws. These regions often offer confidentiality, protecting the identities and transactions of businesses and individuals. This privacy can be a double-edged sword. While it might provide security and competitive advantages, it can also draw attention from regulatory bodies concerned about transparency. Are you prepared to navigate the fine line between privacy and accountability?

Ease Of Business Setup

Setting up a business in a tax haven is typically streamlined and straightforward. Many jurisdictions offer simplified registration processes and fewer bureaucratic hurdles. This ease of setup can be appealing, especially for startups and smaller companies. Yet, it’s essential to ensure that this convenience aligns with your long-term business goals. Will the initial ease of setup translate into sustainable growth and compliance? As you weigh these characteristics, remember that each tax haven has its own unique blend of benefits and challenges. Balancing these factors with your business objectives and ethical considerations can lead to informed and strategic decisions.

Popular Tax Haven Jurisdictions

Tax havens are countries or regions offering low tax rates. They attract businesses seeking to minimize tax burdens. These jurisdictions provide privacy and financial secrecy. Popular tax havens exist worldwide.

Caribbean Islands

The Caribbean hosts several tax havens. Bahamas and Cayman Islands are well-known. They offer zero tax on corporate income. Companies enjoy confidentiality and banking privacy. Offshore accounts are common here. It’s easy to set up a business. These islands attract multinational corporations.

European Nations

Europe has its share of tax havens. Luxembourg and Switzerland are prominent. These countries provide favorable tax conditions. They offer stability and strong financial systems. Corporate tax rates are low, enticing global companies. Privacy laws protect business interests. Many firms prefer these locations for headquarters.

Asian Countries

Asia also features tax-friendly jurisdictions. Singapore and Hong Kong lead the way. They offer competitive tax rates for businesses. These regions boast robust economies. Financial institutions are reliable and secure. Business setup is straightforward. Many enterprises choose Asia for expansion.

Legality Of Using Tax Havens

Using tax havens can be a double-edged sword for businesses. On one hand, they offer significant tax savings; on the other, they pose legal and ethical challenges. Understanding the legality of tax havens is crucial to ensuring your business doesn’t face unexpected legal issues.

Legal Frameworks

Each tax haven operates under its own set of laws and regulations. While these jurisdictions often have favorable tax rates, they also have specific requirements for businesses that operate within their borders. It’s essential to thoroughly understand these legal frameworks to avoid any missteps.

For example, some tax havens may require a physical presence, like an office or a local representative, while others might have more lenient requirements. Knowing these details can prevent legal complications down the line. Have you ever considered what might happen if your business fails to meet these local requirements?

Regulatory Compliance

Regulatory compliance is a critical aspect of using tax havens. Businesses must adhere to both the regulations of the haven itself and the regulations of their home country. This dual compliance can be complex and time-consuming.

Failure to comply with these regulations can result in hefty fines or legal actions. Consider keeping a compliance checklist to ensure all legal obligations are met. Have you thought about the resources your business might need to maintain such a checklist?

International Tax Laws

International tax laws are constantly evolving, impacting how businesses can use tax havens. Countries around the world are increasingly collaborating to close tax loopholes and increase transparency. Staying informed about these changes is vital for any business considering or currently using tax havens.

One example is the OECD’s Base Erosion and Profit Shifting (BEPS) initiative, which aims to prevent tax avoidance through profit shifting. This means your business strategies might need frequent updates to remain compliant. Are you ready to adapt to these ever-changing international tax laws?

Understanding the legality of using tax havens is not just about avoiding penalties. It’s about making informed decisions that align with your business ethics and long-term goals. How will you ensure your business navigates these legal waters successfully?

How Businesses Can Use Tax Havens Legally

To leverage tax havens while staying compliant, businesses should follow these steps:

-

Consult Tax Professionals:

-

Hire experienced tax attorneys or CPAs specializing in international tax law to navigate IRC, FATCA, and FBAR requirements. Firms like Deloitte or EY offer offshore compliance services.

-

-

File Required Forms:

-

Submit Form 8938 (FATCA) for foreign accounts over $50,000.

-

File FinCEN Form 114 (FBAR) for accounts exceeding $10,000 by April 15 annually (automatic extension to October 15).

-

Report CFC income via Form 5471 and GILTI via Form 8992.

-

-

Maintain Transparent Records:

-

Document all offshore transactions, ownership structures, and business purposes to demonstrate legitimacy during IRS audits.

-

-

Choose Reputable Jurisdictions:

-

Select tax havens with stable economies and TIEAs with the U.S., such as Singapore or Bermuda, to reduce scrutiny.

-

-

Establish Legitimate Operations:

-

Set up substantive business activities (e.g., offices, employees) in the tax haven to avoid IRS challenges as a “sham” entity (Gregory v. Helvering, 1935).

-

-

Disclose Offshore Entities:

-

Report foreign corporations, trusts, or partnerships to the IRS and state authorities to avoid penalties for non-disclosure.

-

-

Monitor Global Regulations:

-

Stay updated on OECD, EU, and U.S. anti-avoidance measures, such as the Base Erosion and Profit Shifting (BEPS) framework, which targets tax haven abuse.

-

![]()

Benefits For Businesses

Tax havens offer businesses lower taxes, appealing for cost savings. Legal use requires careful planning to avoid risks. Understanding regulations is crucial for compliance and reputation.

When considering expanding your business or optimizing your financial strategy, you might come across the term “tax haven.” These jurisdictions offer several advantages for businesses, making them an attractive option for many companies. Let’s explore some of the key benefits that businesses can enjoy when operating in tax havens.

Tax Savings

One of the primary appeals of tax havens is the potential for significant tax savings. These regions often have lower tax rates or even no corporate taxes at all. Imagine your business retaining a larger portion of its profits, which can be reinvested for growth or distributed to shareholders. I once consulted with a tech startup that shifted some operations to a well-known tax haven. Their effective tax rate dropped dramatically, allowing them to invest more in research and development. Wouldn’t your business benefit from such financial flexibility?

Asset Protection

In the unpredictable world of business, protecting your assets is crucial. Tax havens typically offer robust legal frameworks that safeguard your assets from creditors and legal claims. This can be a game-changer if your business operates in volatile markets. Consider a retail company facing potential litigation in its home country. By relocating assets to a tax haven, the company was able to shield its resources and continue operations without disruption. Have you thought about how asset protection might secure your business’s future?

Privacy Advantages

Privacy is another major draw for businesses considering tax havens. These jurisdictions often have strict confidentiality laws, ensuring that business and financial information is kept private. This can be particularly appealing if your business operates in a highly competitive industry. A colleague in the finance sector once mentioned how his firm benefited from the privacy policies of a tax haven. They could conduct sensitive negotiations without fear of leaks or external pressure. How could enhanced privacy improve your business strategy? In weighing the benefits of tax havens, it’s essential to consider how these advantages align with your business goals. Whether it’s tax savings, asset protection, or privacy, understanding these benefits can help you make informed decisions. What steps will you take to optimize your business’s financial strategy?

Risks And Challenges

Using tax havens can offer businesses financial benefits. But these come with risks and challenges. Businesses must navigate complex legal landscapes. They face reputational and compliance issues. Understanding these risks is crucial for any business considering tax havens.

Legal Risks

Tax havens often have unclear regulations. This can lead to legal trouble. Businesses may face fines or penalties. Governments continuously change tax laws. This makes compliance tricky. Legal risks can also include criminal charges. Companies need to stay informed and compliant.

Reputational Damage

Using tax havens can harm a business’s reputation. People may see it as unethical. This can lead to loss of trust. Customers and partners may turn away. Negative media coverage can arise. Businesses must weigh the benefits against potential backlash. Protecting reputation is key.

Compliance Issues

Maintaining compliance is challenging. Tax havens often have complex requirements. Businesses must ensure proper reporting. Failing to do so can lead to audits. Compliance costs can be high. Companies need strong internal controls. Staying compliant helps avoid penalties.

Impact On Global Economy

Tax havens significantly influence the global economy. These jurisdictions offer low or no tax rates, attracting businesses seeking tax savings. While businesses benefit, tax havens can create challenges for countries worldwide. They impact government revenues, economic fairness, and regulatory measures.

Tax Revenue Loss

Countries face major tax revenue losses due to tax havens. Businesses shift profits to these low-tax jurisdictions, reducing taxable income in their home countries. Governments struggle to fund public services. Education, healthcare, and infrastructure may suffer due to reduced funds. This revenue loss affects economic growth and stability.

Economic Inequality

Tax havens contribute to growing economic inequality. Wealthy individuals and corporations benefit from tax savings. Meanwhile, average citizens pay higher taxes to cover budget shortfalls. This situation widens the gap between rich and poor. Economic inequality can lead to social unrest and instability.

Regulatory Responses

Governments and organizations respond to the challenges posed by tax havens. They implement regulations and policies to curb tax avoidance. International cooperation aims to increase transparency and accountability. Efforts include sharing financial information and imposing stricter tax laws. These measures seek to ensure fair taxation globally.

Future Of Tax Havens

The future of tax havens is becoming a hot topic. Global economies are changing. The way businesses handle taxes is under scrutiny. Many countries want to close loopholes. They aim for fair tax practices. Businesses must adapt to these changes. Understanding the future of tax havens is vital. It helps in making informed decisions.

Regulatory Changes

New regulations are emerging. They target tax avoidance. Governments are closing gaps. These gaps once allowed easy tax evasion. Rules are getting stricter. Compliance is crucial for businesses. Failing to comply can lead to penalties. Companies must stay updated. They should monitor regulatory changes closely.

Technological Impact

Technology plays a big role. It affects how tax havens operate. Digital tools are tracking transactions. Data is more accessible now. This makes hiding wealth harder. Transparency is increasing. Technology exposes hidden assets. Businesses must embrace tech. They should use it for compliance.

Global Cooperation

Countries are working together. They share tax information. This cooperation is growing. It aims to prevent tax evasion. International agreements are forming. They ensure fair tax practices. Businesses face global scrutiny. They must align with global standards. Cooperation benefits honest businesses.

Case Studies

-

Apple in Ireland: Apple used Ireland’s low tax rates to channel profits, saving billions. However, a 2016 EU ruling ordered Apple to pay €13 billion in back taxes, highlighting international risks (European Commission v. Apple, 2016).

-

Panama Papers Fallout: The 2016 leak exposed thousands of offshore entities, leading to IRS investigations and penalties for U.S. taxpayers failing to report accounts.

-

Legitimate Use: A U.S. tech startup establishes a Singapore subsidiary for Asia-Pacific operations, reporting all income via Form 5471 and complying with FATCA, avoiding penalties.

Frequently Asked Questions

What Is A Tax Haven?

A tax haven is a country or territory offering low or no taxes, attracting individuals and businesses seeking tax benefits. These jurisdictions provide financial privacy, which can lead to legal and ethical concerns. Tax havens can impact global economies and are often scrutinized for facilitating tax avoidance.

Are Tax Havens Legal For Businesses?

Tax havens are legal, but businesses must navigate complex international laws. Using tax havens can raise ethical issues and compliance risks. Companies must ensure adherence to all relevant regulations to avoid penalties. Proper legal guidance is crucial for businesses considering tax haven strategies.

Why Do Businesses Use Tax Havens?

Businesses use tax havens to reduce tax liabilities and increase profits. By operating in these jurisdictions, companies can benefit from favorable tax regimes. Additionally, tax havens offer financial privacy, which can be attractive for businesses seeking confidentiality. However, ethical considerations and regulatory compliance are important factors.

What Risks Do Tax Havens Pose To Businesses?

Tax havens pose various risks, including legal penalties and reputational damage. Businesses may face scrutiny from governments and watchdogs. Non-compliance with international tax laws can lead to fines and sanctions. Companies should carefully assess these risks before using tax havens for operations.

Conclusion

Tax havens offer tempting benefits for businesses. Lower taxes. Confidentiality. Yet, risks loom. Legal complications can arise. Regulatory changes might impact operations. Businesses must weigh pros and cons. Conduct thorough research before proceeding. Consult legal experts for guidance. Ethical considerations matter too.

Transparency is important. Reputation can suffer if ignored. Be cautious with decisions. Tax havens aren’t for everyone. Responsible strategies are key. Understand the risks fully. Choose wisely for long-term success.

References

- Internal Revenue Code, 26 U.S.C. §§ 61, 7201, 951, 951A, 1471 et seq. (2025).

- Bank Secrecy Act, 31 U.S.C. § 5311 et seq. (2025).

- U.S. v. Zwerner, Case No. 13-13066-CIV-MARRA (S.D. Fla. 2014).

- Cal. Rev. & Tax. Code § 19141.6 (2025).

- Gregory v. Helvering, 293 U.S. 465 (1935).

- European Commission v. Apple, Case T-892/16 (2016).

- Organization for Economic Cooperation and Development. (2025). Common Reporting Standard. Retrieved from https://www.oecd.org.

- IRS. (2025). Foreign Account Tax Compliance Act (FATCA). Retrieved from https://www.irs.gov.

- FinCEN. (2025). Report of Foreign Bank and Financial Accounts (FBAR). Retrieved from https://www.fincen.gov.

Disclaimer: The content on this page is for general information only and should not be considered legal advice. We work hard to provide accurate and up-to-date details, but we can't guarantee the completeness or accuracy of the information. Laws and rules change often, and interpretations may vary. For specific advice, always consult a qualified legal expert. We are not liable for any actions you take based on this information. If you spot any errors or outdated content, please contact us, and we’ll update it as soon as possible.